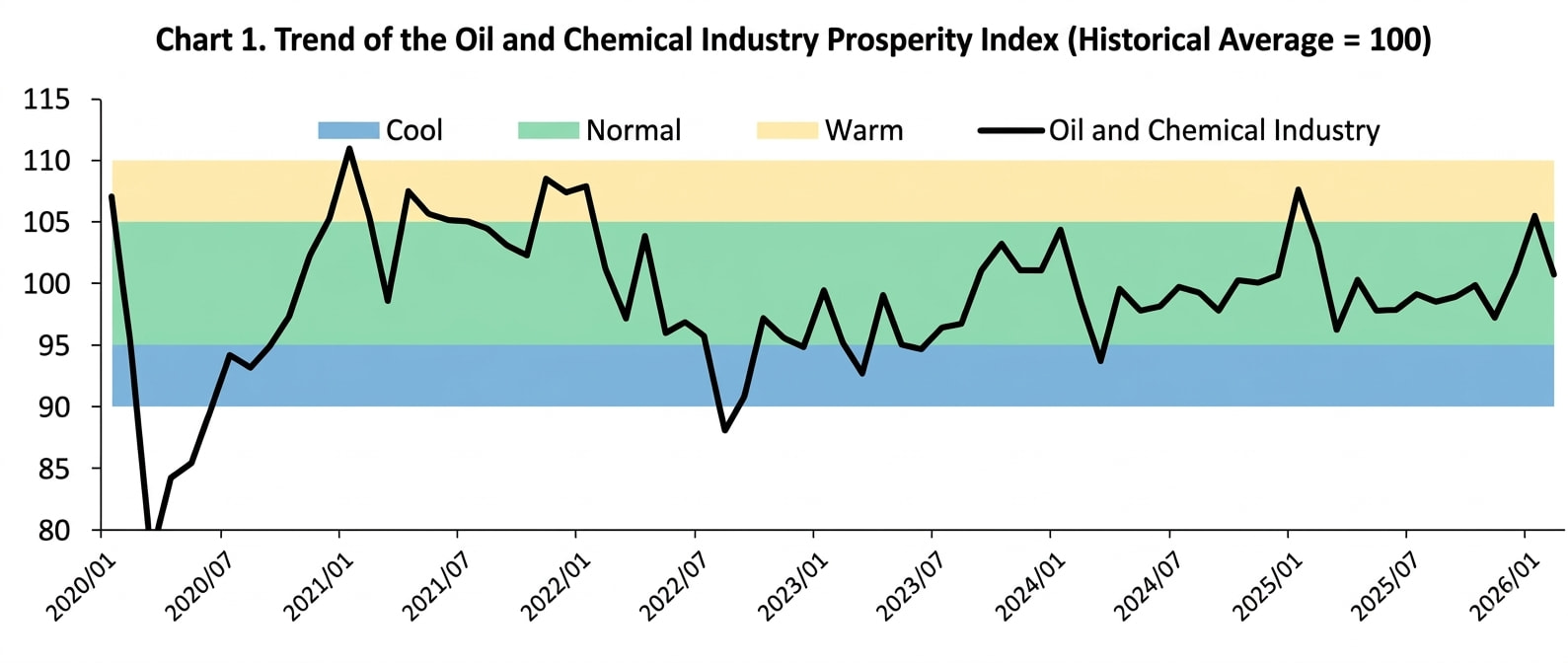

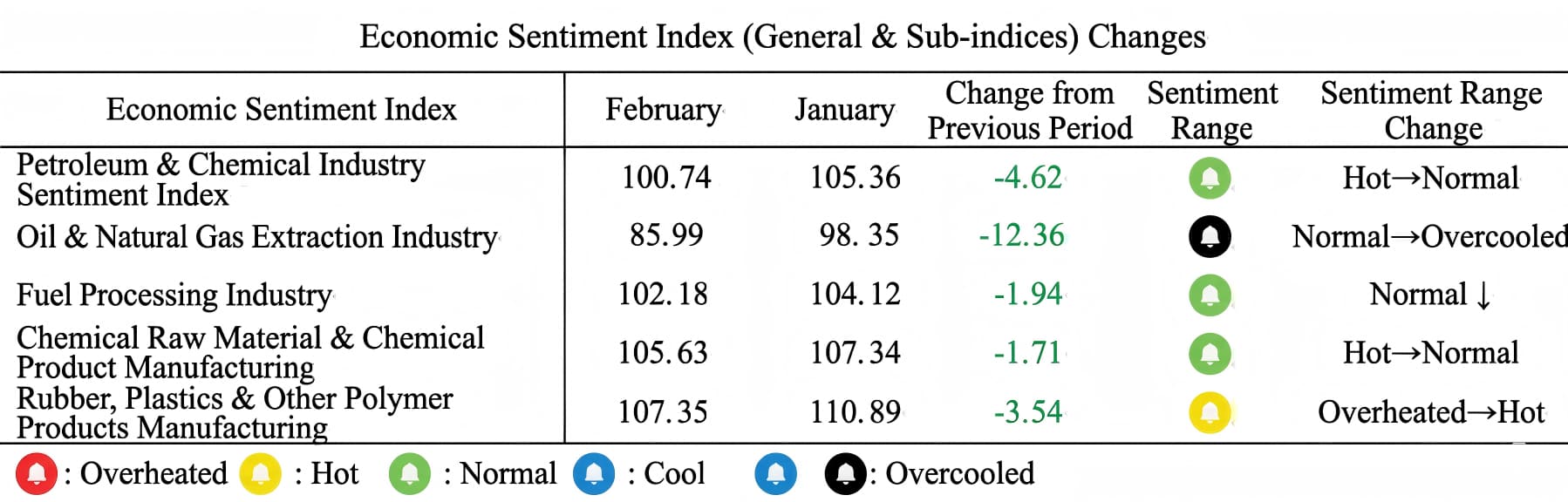

1. Обзор Индекса процветания нефтяной и химической промышленности

Индекс делового климата для нефтегазодобывающей отрасли составил 85,99, что на 12,36 процентных пункта меньше, чем в предыдущем месяце. В последние два месяца, под влиянием геополитической напряженности, цены на нефть продолжали расти. Однако текущие цены на нефть сопряжены со значительной премией за риск, а в сочетании с предыдущим шестимесячным периодом «снижения цен и сокращения прибыли» компании ставят под сомнение устойчивость восстановления цен на нефть и сохраняют осторожность в принятии решений о производстве. Изменения в оборачиваемости запасов отражают завершение поэтапного сокращения запасов в январе. В условиях роста цен на нефть компании могут сохранять запасы в ожидании дальнейшего повышения цен, а в сочетании с приближающимся праздником Весны ожидается снижение спроса со стороны потребителей, что приведет к замедлению сокращения запасов.

Индекс делового климата для отрасли переработки топлива составил 102,18, что на 1,94 процентных пункта меньше, чем в предыдущем месяце. В отрасли переработки топлива наблюдаются незначительные различия между продуктами. Потребление дизельного топлива конечными потребителями достигло нового минимума по сравнению с традиционным годовым минимумом, что подчеркивает дисбаланс между спросом и предложением. В то время как спрос на бензин поддерживался краткосрочными поездками во время праздника Весны, после него он быстро снизился.

Индекс благосостояния химической отрасли, занимающейся производством сырья и химической продукции, составил 105,63, что на 1,71 процентных пункта меньше, чем в предыдущем месяце. Умеренное восстановление цен на нефть в нефтеперерабатывающей отрасли пока не привело к росту стоимости сырья, а цены на химическую продукцию в перерабатывающей отрасли остаются относительно стабильными, поддерживая рентабельность. Однако производственная активность снизилась из-за остановок и технического обслуживания предприятий во время праздника Весны, а объемы новых закупок в перерабатывающей отрасли сократились, что привело к накоплению запасов готовой продукции и снижению индекса благосостояния отрасли.

Индекс процветания обрабатывающей промышленности для резинаИндекс процветания отрасли по пластмассам и другим полимерным изделиям составил 107,35, что на 3,54 процентных пункта меньше, чем в предыдущем месяце. В январе процветание отрасли выросло благодаря преимуществам в стоимости сырья и сезонному спросу на создание запасов. Однако в начале февраля темпы создания запасов замедлились в преддверии Праздника весны, а восстановление спроса после праздников во второй половине месяца было медленным. Сокращение новых заказов привело к увеличению запасов, что вызвало снижение индекса процветания отрасли. В настоящее время отрасль находится в фазе перераспределения запасов, и ее будущее процветание будет зависеть от восстановления внутреннего и международного спроса.

2. Анализ проблемных зон и перспективы на будущее.

2.1 Обострение геополитической напряженности на Ближнем Востоке и рост цен на нефть

В феврале геополитическая напряженность на Ближнем Востоке резко обострилась, став основной причиной роста цен на нефть. 28 февраля США и Израиль нанесли авиаудары по Тегерану, столице Ирана, после чего Корпус стражей исламской революции Ирана объявил о закрытии Ормузского пролива, жизненно важного глобального маршрута транспортировки нефти. Это событие ознаменовало переход от «торговых ожиданий» к «торговой реальности» в геополитическом конфликте, вызвав серьезные опасения рынка по поводу перебоев в поставках нефти. В результате цены на нефть быстро выросли, а геополитическая премия за риск значительно увеличилась. По оценкам, текущие цены на нефть уже включают в себя премию за риск в размере примерно 8-10 долларов за баррель. Кроме того, значительная часть нефтехимической продукции, такой как Поливиниловый спирт (ПВА), Поливинилбутиральная смола (ПВБ)и мазут ежегодно транспортируются через Ормузский пролив; продолжение конфликта неизбежно повлияет на цены на эти сопутствующие товары.

2.2 Вялое производство, высокое потребление и медленное пополнение запасов

В этом году, благодаря самым продолжительным в истории праздникам Весны, спрос на межрегиональные поездки для посещения родственников и туризма был сконцентрирован, что привело к частым пикам движения на автомагистралях и напрямую увеличило потребление бензина. Однако, в отличие от всплеска внутренних поездок, промышленная и инфраструктурная деятельность в целом замедлилась во время Праздника Весны, а потребление дизельного топлива вошло в традиционный годовой минимум. Ежедневное потребление значительно снизилось по сравнению с предыдущим периодом, а давление на запасы на нефтеперерабатывающих заводах и в обществе продолжало расти.

В период весеннего фестиваля потребительский рынок демонстрировал оживленные продажи бытовой техники и цифровой электроники, что временно повысило спрос на соответствующее нефтехимическое сырье в отраслях производства резины, пластмасс и других полимерных изделий, улучшив ожидания отрасли относительно показателей рынка после праздников. Однако с окончанием праздников намерения пополнять запасы ослабли, и дистрибьюторы в целом вступили в цикл сокращения запасов, что привело к незначительному замедлению новых заказов для нефтехимических компаний. В целом, февраль характеризовался активным туризмом, вялым производством, высоким потреблением и медленным пополнением запасов, что наглядно демонстрирует логику дифференциации в нефтехимической отрасли и общую коррекцию ее общего процветания.

3. Перспективы развития нефтяной и химической промышленности

В марте 2026 года на нефтегазовую и химическую промышленность продолжат влиять макроэкономические факторы, издержки и спрос. На макроуровне Всекитайское собрание народных представителей и Всекитайское политическое консультативное собрание Китая (ВСНП и ВПКК) опубликуют ряд политических сигналов, указывающих на рыночные тенденции в 2026 году. Что касается цен на нефть, если геополитическая напряженность на Ближнем Востоке не ослабнет и Ормузский пролив останется закрытым, ожидается, что в марте сохранятся премии за риск на рынке нефти и высокая волатильность, что потенциально может привести к дальнейшему росту цен. Со стороны спроса возобновление работы и производства в перерабатывающих отраслях после Весеннего фестиваля происходило медленно, и рост цен на нефть еще больше снизил прибыль нефтехимической промышленности. Компании-конечные потребители сохранили только необходимые закупки и не имели мотивации для концентрированного пополнения запасов. Ключевыми факторами восстановления процветания отрасли являются возможность успешного преобразования ранее существовавшего спроса на пополнение запасов со стороны предприятий среднего и нижнего звена, основанного на ценовых преимуществах, в потребление конечными потребителями, а также возможность наступления традиционного пикового сезона «Золотого марта и Серебряного апреля» в запланированные сроки. На основе всесторонней оценки исторических сезонных закономерностей и текущих данных ожидается, что индекс процветания нефтехимической отрасли в марте покажет тенденцию к снижению.

Веб-сайт: www.elephchem.com

WhatsApp: (+)86 13851435272

Электронная почта: admin@elephchem.com

Поддерживается сеть IPv6

Поддерживается сеть IPv6