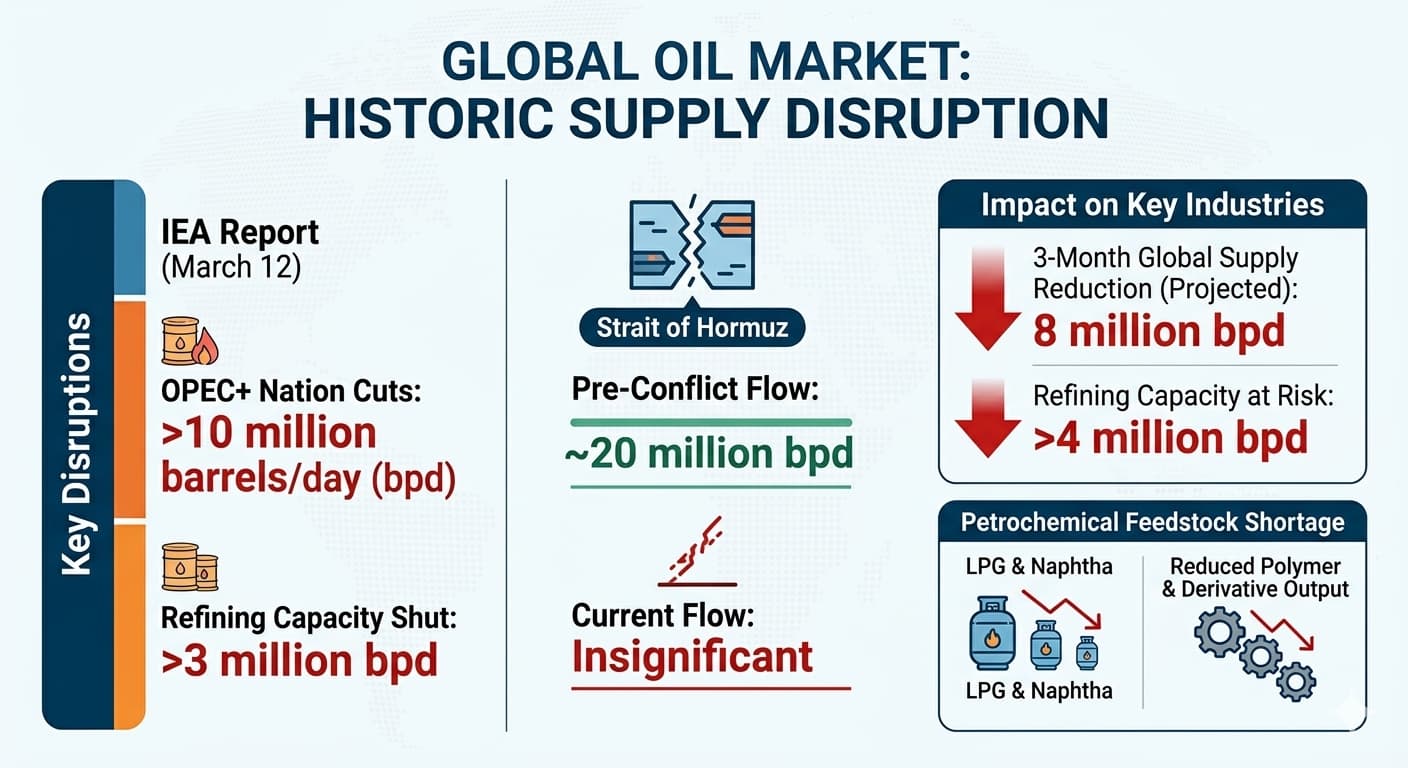

12 марта Международное энергетическое агентство (МЭА) в своем последнем ежемесячном отчете заявило, что мировой рынок нефти столкнулся с самыми серьезными перебоями в поставках за всю историю из-за продолжающегося конфликта на Ближнем Востоке. Судоходство через Ормузский пролив практически полностью парализовано, а хранилища почти заполнены, поэтому государства Персидского залива вынуждены сократить добычу нефти как минимум на 10 миллионов баррелей в сутки, а мощности нефтеперерабатывающих заводов — более чем на 3 миллиона баррелей в сутки.

До конфликта через Ормузский пролив транспортировалось около 20 миллионов баррелей сырой нефти и нефтепродуктов; сейчас эта цифра упала до незначительного уровня. В докладе говорится, что если судоходство не возобновится в ближайшее время, дефицит предложения сырой нефти в мире еще больше увеличится. В докладе прогнозируется сокращение мирового предложения нефти на 8 миллионов баррелей в сутки в марте, при этом под угрозой окажется более 4 миллионов баррелей в сутки перерабатывающих мощностей. Рынки дизельного топлива и авиационного топлива особенно уязвимы из-за блокировки экспорта. В докладе также отмечается, что недостаток доступного сырья ограничит производство в других регионах, что потенциально может привести к дефициту поставок вплоть до 2026 года. В 2025 году производители Персидского залива экспортировали 3,3 миллиона баррелей переработанных нефтепродуктов и 1,5 миллиона баррелей сжиженного нефтяного газа (СНГ) в сутки.

В докладе показано, что, хотя увеличение добычи в странах, не входящих в ОПЕК+, таких как Казахстан и Россия, ослабило напряженность в отношении поставок, этого улучшения недостаточно для полного компенсации давления на мировой рынок. Международное энергетическое агентство (МЭА) прогнозирует, что мировые поставки нефти увеличатся на 1,1 миллиона баррелей в сутки в 2026 году. Этот рост в основном обусловлен увеличением добычи в странах, не входящих в ОПЕК+. Однако следует отметить, что масштабы сокращения поставок нефти зависят от продолжительности конфликта и степени нарушения торговых потоков.

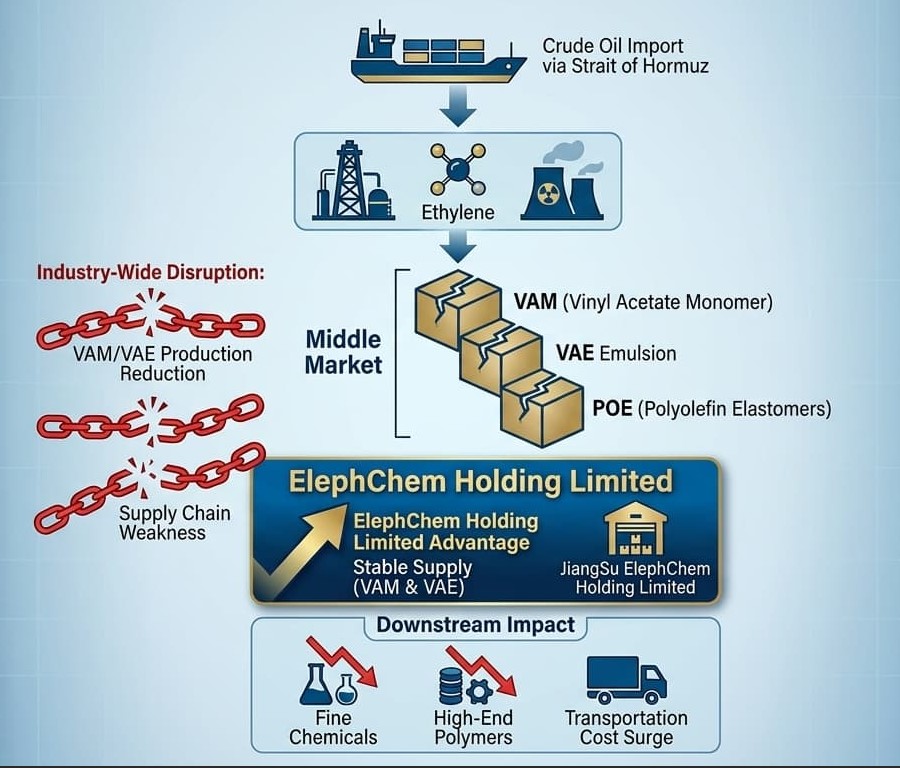

В отчете прогнозируется, что отмена рейсов и перебои в поставках сжиженного нефтяного газа на Ближнем Востоке приведут к снижению спроса на нефть на 1 миллион баррелей в сутки в марте и апреле по сравнению с предыдущими прогнозами. Военный конфликт в Иране и прилегающих регионах не только потряс мировой энергетический рынок, но и значительно повлиял на международную индустрию этилена и всю ее цепочку поставок. Его негативные последствия распространяются от нефтедобычи, а также на основные промежуточные продукты, такие как этилен и другие. ВАМ (Винилацетатный мономер)а также далее по цепочке поставок к тонким химическим веществам, таким как эмульсии VAE. От Европы до Азии стремительный рост цен на сырье и риск сбоев в цепочке поставок вызывают широкую обеспокоенность в отрасли.

Глобальный кризис в цепочке поставок этилена

Напряженность в Иране напрямую влияет на глобальную цепочку поставок этилена. Будучи вторым по величине производителем этилена на Ближнем Востоке, Иран обладает производственными мощностями в размере приблизительно 7,88 млн тонн, что составляет 23% от общего объема производства в регионе. Сбои в производстве такого масштаба напрямую увеличивают глобальные издержки на химическую продукцию. Ормузский пролив, являющийся важнейшим узким местом для морских перевозок энергоносителей, обеспечивает около 20% мирового морского транспорта сырой нефти и значительную долю поставок химической продукции. После объявления Ираном о закрытии пролива опасения по поводу логистических сбоев немедленно вылились в премию за рыночный риск.

Примерно 11–15% мирового предложения этилена и полиэтилена напрямую затронуты этим конфликтом, и цены на соответствующие химические вещества уже начали расти. В Европе переговоры по мартовским ежемесячным контрактам на этилен зашли в тупик из-за резкого роста цен на нефть: первоначально ожидаемое повышение на 35 евро/тонну быстро сменилось ожиданиями в 50–60 евро/тонну, что отражает широко распространенные на рынке опасения по поводу перебоев в поставках. Азиатские рынки также резко отреагировали: цены на нафту взлетели до многомесячных максимумов. В Китае последовали аналогичные изменения на внутреннем рынке фьючерсов на полиолефины (ПП/ПЭ), при этом спотовый рынок перешел от планового пополнения запасов к защитному накоплению запасов.

Нисходящие цепочки поставок испытывают давление.

Этот кризис быстро распространяется по всей цепочке поставок: нефть → этилен → винилацетат → винилацетат. Из-за крайне ограниченного предложения этилена производство винилацетата (VAM) напрямую ограничено нехваткой сырья, и его рыночная цена рискует резко вырасти. Поскольку винилацетат является основным продуктом переработки винилацетата, стабильность цепочки поставок крайне важна. ВАЭ (эмульсия сополимера винилацетата и этилена) серьезно пострадала отрасль. В целом, ожидается, что по мере перекладывания затрат на VAM, эмульсия VAE Цены неизбежно вырастут. Однако, на фоне широко распространенных в отрасли ограничений на производстве и значительного сокращения ожидаемого объема производства VAE из-за недостаточного предложения VAM, компания JiangSu ElephChem Holding Limited способна обеспечить стабильные поставки VAM и продуктов переработки VAE.

Веб-сайт: www.elephchem.com

WhatsApp: (+)86 13851435272

Электронная почта: admin@elephchem.com

Поддерживается сеть IPv6

Поддерживается сеть IPv6